Sections of the site

Editor's Choice:

- Which pair is suitable for twins?

- Transport tax accrued (accounting entries) Transport tax rate in 1s 8

- Characteristics of a Taurus woman by zodiac sign: a gorgeous and sophisticated lady Taurus girls in relationships

- Love horoscope for Libra - rat Horoscope for April Libra water rat and

- I dreamed that I had a big belly

- Why do you dream about your parents getting divorced? I had a dream that my parents were getting divorced.

- Slavic runes, designation and interpretation

- Pisces will be helped by a person from the past, and lions will overcome the trials of fate

- Functions of the general agent for servicing public debt

- Other income - what is it?

Advertising

| Calculation of transport tax (accounting entries). Transport tax accrued (accounting entries) Transport tax rate in 1s 8.3 |

|

Transport tax accrued - postingsin accounting for this operation may be different. You will learn from our article what the reflection in the postings of certain accounting accounts depends on, and you will also be able to understand how transport tax is calculated and taken into account. Explanation of the concept of transport taxTransport tax is regional. Its rates are regulated by regional authorities, but they should not differ more than 10 times from the rate specified in the Tax Code (Article 28 of the Tax Code of the Russian Federation). This tax must be paid by all owners of transport (Article 357 of the Tax Code of the Russian Federation) - legal entities and individuals who have at their disposal (by right of ownership or ownership) transport registered in accordance with the laws of the Russian Federation. Read about the nuances of vehicle registration and the tax consequences of its absence in the article “The lack of registration of a vehicle will not exempt you from transport tax” . How is transport tax calculated?The obligation to independently calculate tax is assigned only to legal entities. For individual entrepreneurs and individuals, this calculation is made by the Federal Tax Service (Clause 1 of Article 362 of the Tax Code of the Russian Federation). The calculation of transport tax involves the application of a rate to the tax base, taking into account the time the transport is in the payer’s ownership. In some cases, an increasing coefficient is also applied (clause 2 of Article 362 of the Tax Code of the Russian Federation). Please note that the tax must be paid not by the one who uses the vehicle, but by the one who owns it. Even if the owner has issued a power of attorney to drive the vehicle, the authorized person does not pay tax. Tax is calculated for the full month during which the vehicle is owned by the payer. Until 2016, the month of registration and deregistration was considered a full month for which the tax was calculated. Starting from 2016, the registration month is considered complete if the vehicle is registered before the 15th day inclusive. The month of deregistration is considered complete if the object is deregistered after the 15th day. Tax accounting of transport taxTo calculate income tax, transport tax is taken into account in other expenses that are associated with production and sales (clause 1 of Article 264 of the Tax Code of the Russian Federation). When calculating the simplified tax system with the object “income”, the amount of transport tax is not taken into account, since expenses do not matter for its calculation (clause 1 of article 346.18 of the Tax Code of the Russian Federation). When simplified with the object “income minus expenses,” transport tax is included in expenses (Article 346.16 of the Tax Code of the Russian Federation). Unpaid transport tax cannot be taken into account when calculating the simplified tax system. Read more about tax under the simplified tax system in the article “Transport tax under the simplified tax system: calculation procedure, terms, etc.” . As for UTII, the amount of imputed tax does not depend on the amount of transport tax, since its calculation is done without taking into account income received and expenses incurred. If the payer uses OSNO and UTII together and transport is used in both taxation regimes, the tax amount must be divided. When using transport in only one of the modes, such separation is not necessary. If transport was used in activities related to OSNO, it can be taken into account to reduce income tax, if with UTII, the imputed tax cannot be reduced. To correctly distribute the transport tax between the two regimes, you need to calculate what part is the income for each type of activity. To calculate the portion of income under OSNO, you must do the following: divide the amount of income under OSNO by income from all types of activities. The transport tax related to OSNO is determined by multiplying the amount of transport tax and the share of income received from OSNO. Transport tax related to activities on UTII is calculated in the same manner, using in this calculation the amount of income received on UTII. The sum of the results obtained from both calculations should give the total amount of accrued tax. ResultsIndependent calculation of transport tax is the prerogative of legal entities. They also keep records of tax accrual and payment, reflecting it in accounting entries. In accounting, tax usually forms expenses for activities performed. In tax accounting, it is included in costs that reduce the base for income tax or simplified tax system with the object “income minus expenses.” When combining taxation regimes, the tax may be distributed. Step 1. Setting up 1C 8.3 for transport taxTo set up transport tax in 1C 8.3: payment deadlines and reflection of expenses, you must specify the necessary settings in the Directories - Transport Tax section. Here you can set the payment procedure and methods for reflecting expenses, while in 1C 8.3 you can set your own settings for each organization: Step 1.1. Deadlines for payment of transport tax

Step 1.2. Ways to reflect expensesMethods for reflecting expenses in 1C 8.3 can be entered both generally for all organizations, and in the context of each organization. And similarly for all vehicles or for a specific one. Please note:

Don't forget to indicate the analytics for the account:

Step 2. Receipt of the vehicleA vehicle is a fixed asset, therefore, like any other fixed asset, the acquisition is recorded in the document Receipt of equipment in the fixed assets and intangible assets section:

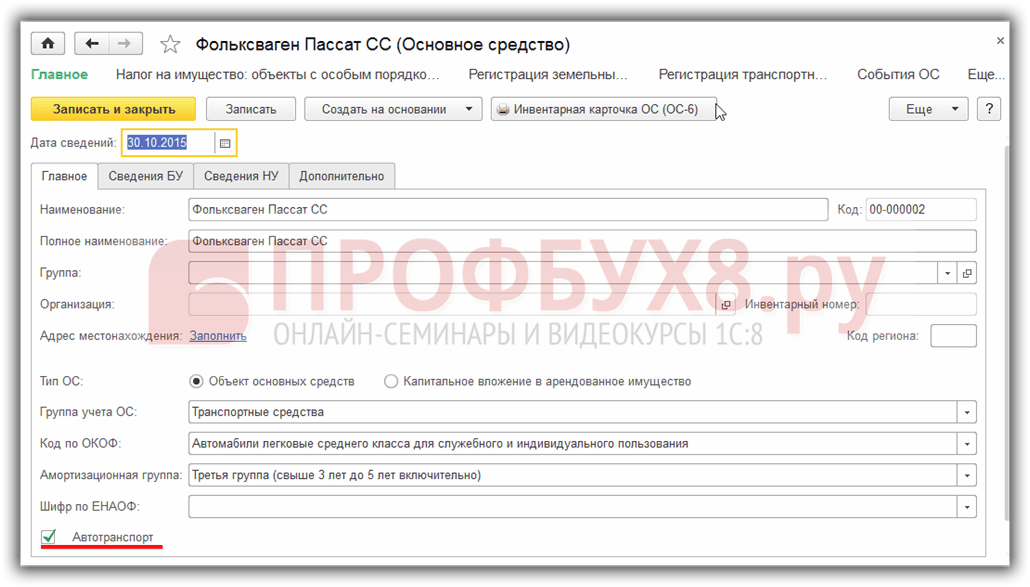

Step 2.1. Filling out the directory Fixed assetsSince filling out a document with a vehicle is not very different from, let’s look at the nuances of filling out a vehicle in more detail in the Fixed Assets directory. When filling out the form in 1C 8.3, indicate:

Step 3. Vehicle registration in 1C 8.3You can reflect the fact of vehicle registration with the traffic police using the Vehicle Registration command in the Directories - Transport Tax section - select Vehicle Registration:

or a similar item in the Fixed Assets directory:

With this register of information in 1C 8.3 you can register a vehicle with the State Traffic Safety Inspectorate, as well as deregister:

In registration we indicate:

Step 4. Registering the vehicleAcceptance of vehicles for registration in 1C 8.3 is registered with the document Acceptance for accounting of fixed assets in the paragraph OS and intangible assets:

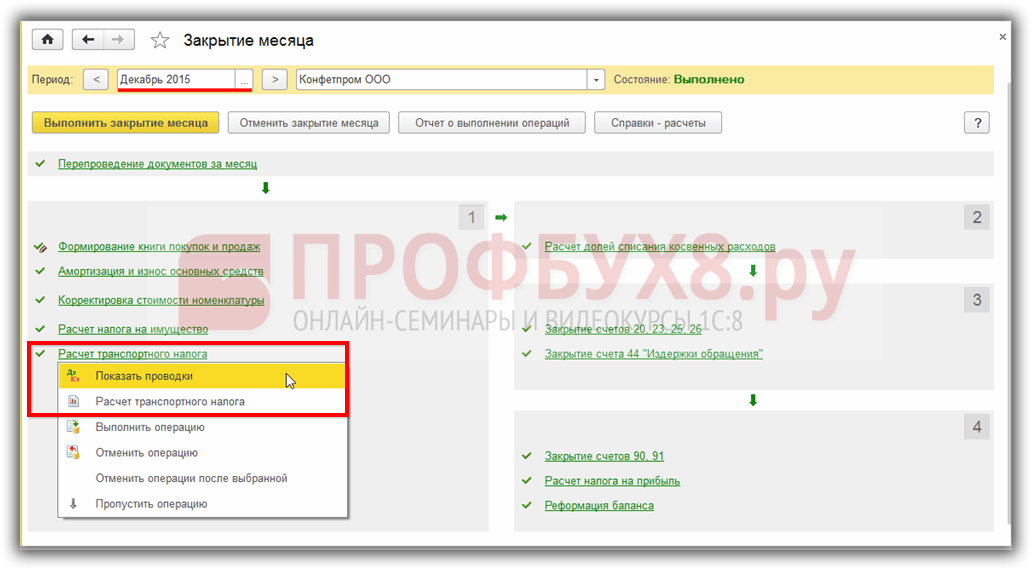

Step 5. Calculation of transport tax in 1C 8.3 AccountingTransport tax in 1C 8.3 is calculated at the end of the month at the end of the year - December. You can start Month Closing processing from the Operations – Month Closing section. Postings for transport tax in 1C 8.3, as well as the report, can be viewed by clicking on the link Calculation of transport tax:

Costs for transport tax in 1C 8.3 are allocated to the account specified in the program settings in the methods of reflecting expenses:

To decipher the tax amounts in 1C 8.3, we will use the Help-calculation of transport tax report. The report allows you to timely check all data on transport tax before generating a declaration:

Starting with release 3.0.32.6 in the 1C 8.3 Accounting program, automatic calculation of transport tax is possible. How to set up for automatic tax calculation in 1C, see our video:

Step 6. Transport tax declarationStep 6.1. Filling out the declarationA transport tax declaration in 1C 8.3 can be prepared in the Reports section - Regulated reports. Next, click on the Create button and select the Transport Tax Declaration (annual) report:

It is necessary to check the taxpayer's information on the title page. If some data in 1C 8.3 is not filled in automatically, then you need to check the completion of the Organization directory. To automatically fill out sections 1 and 2, click Fill. Light green fields are filled in automatically with the possibility of manual adjustment:

Step 6.2. Checking the declarationBy clicking the Check button in 1C 8.3, you can check the completion of the report. If there are any errors, the program will show it:

Step 6.3. Printing and downloading the declarationIn 1C 8.3 Accounting, you can immediately print a transport tax return from the report or first view it electronically, using the appropriate options from the Print command:

You can also use 1C-Reporting to immediately send a declaration from 1C 8.3 to regulatory authorities or use the Upload and send button using a third-party program.

Step 7. DeregistrationA vehicle can be deregistered for many reasons. For example, the sale or write-off of vehicles, which in 1C 8.3 are documented with standard documents for asset accounting. Published 08/23/2016 07:44 Views: 6038Quite often, readers of our site ask the question: why is transport tax not automatically calculated in 1C? We accepted the car for registration as a fixed asset, filed everything correctly, but the program does not want to calculate the transport tax. And sometimes the opposite situation occurs, when the vehicle has already been sold or written off, but the program still “sees” it and takes it into account in calculations. As a rule, the reason for such errors lies in the lack of registration or deregistration of the vehicle in the program. In this article, first of all, we will look at how to reflect vehicle registration in the 1C: Enterprise Accounting 8 edition 3.0 program. Why do you need to enter any additional documents besides the actual acceptance of fixed assets for accounting? Let's remember: an enterprise becomes a transport tax payer at the moment the vehicle is registered with the State Traffic Safety Inspectorate, and it is precisely this fact that we must additionally reflect in the program, because in terms of time this event does not always coincide with the acceptance of the fixed asset for accounting. So, open the section “Directories”, “Taxes”, “Transport tax”, “Vehicle registration”

Click the “Create” button and create a vehicle registration

In the document that opens, fill in the empty fields:

Record and close

We figured out how to register a vehicle upon purchase. However, it must be remembered that when we sell a vehicle, we must deregister it so that transport tax is no longer charged. To do this, we also go to the section “Directories”, “Taxes”, “Transport tax”, “Registration of vehicles”. And click on the “Create” button and select “Deregistration”

Organizations that have vehicles are required to submit tax returns and tax calculations for advance payments of transport tax to the tax authorities at the location of the vehicles. S.A. talks about how to prepare tax reports for transport tax using the 1C: Accounting 8 program. Kharitonov, Doctor of Economics, Professor of the Financial Academy under the Government of the Russian Federation. Tax reporting on transport taxAn organization on whose balance sheet there are vehicles (cars and trucks, buses, airplanes, boats, etc.), in accordance with Chapter 28 “Transport Tax” of the Tax Code of the Russian Federation, is recognized as a taxpayer for transport tax, and the vehicles themselves are an object of taxation transport tax. As a transport tax payer, the organization is obliged to:

At the end of each reporting period, transport tax reporting is submitted no later than the last day of the month following the expired reporting period. At the end of the tax period, transport tax reporting is submitted no later than February 1 of the year following the expired tax period. Thus, at the end of the third quarter of 2008, an organization recognized as a taxpayer of transport tax must submit to the tax authority no later than October 31, 2008 a tax calculation for advance payments for transport tax. Tax accounting of vehicles in "1C: Accounting 8"Preparation of tax calculations in the general case is a non-trivial task. In order to solve it correctly, it is necessary to study not only Chapter 28 of the Tax Code of the Russian Federation “Transport Tax”, but also Order No. 48n of the Ministry of Finance of Russia dated March 23, 2006, which approved the tax calculation form for advance payments for transport tax and recommendations for filling it out, and for preparing a tax return - order of the Ministry of Finance of Russia dated April 13, 2006 No. 65n. At the same time, the task of filling out tax forms for transport tax can be significantly simplified, while saving time, if you use the corresponding regulated report of the 1C: Accounting 8 program for this purpose. The report allows you to create a tax calculation (tax return) almost automatically based on vehicle tax records. Tax accounting of vehicles in the 1C: Accounting 8 program includes registration in the information base of information about the registration of the vehicle and the deregistration of the vehicle. An information register is designed to store tax accounting data for vehicles. (menu OS -> Vehicle registration). The register is periodic (the frequency of register entries is within a day) and has an independent recording mode. The latter means that entries in the register are made “manually” in the mode of direct work with this object. We will consider the procedure for tax accounting of vehicles and drawing up tax calculations for advance payments for transport tax using the data from the following example. ExampleThe organization "White Acacia" has two cars on its balance sheet. Entering information about vehicle registrationWhen registering a vehicle in the information register Vehicle registration you must enter a record with the form (Fig. 1). Rice. 1 Moreover, in the form of a record Vehicle registration are indicated (Fig. 2): Entering benefit informationIn general, the laws of the constituent entities of the Russian Federation may provide benefits for vehicles. Information about benefits is indicated in the form Tax benefit, which opens by clicking on the “value” of the attribute of the same name in the form Vehicle registration. In this case, the type of transport tax benefit is set using the switch: For all benefits, the program enters benefit code 20200 (in accordance with Appendix No. 3 to the Procedure for filling out the tax return form for transport tax, approved by Order of the Ministry of Finance of Russia dated April 13, 2006 No. 65n). If the law of a constituent entity of the Russian Federation changes the tax rate, the amount and procedure for providing tax benefits, the information register Vehicle registration You must enter a new entry “registration of the vehicle”. In the Date of registration of this entry, you should indicate the date from which the changes come into force. Entering information about deregistration of a vehicleWhen deregistering a vehicle from the register of information Vehicle registration a record is entered with the form (Fig. 8). Example (continued)The Toyota Corolla car, registered with the tax authorities at the location of the organization, was deregistered on August 12, 2008 due to the sale. Rice. 8 In such situation Deregistration indicated (Fig. 9):

Transport tax rates are established by the law of the subject of the Russian Federation at the location of the car - registration of the organization or its division. They depend on engine power and vehicle category. Finding the current rate for your region takes time. But now users of “1C: Accounting 8” (rev. 3.0) do not need to bother searching - starting from version 3.0.42.63, the tax rate is selected automatically. The transport tax rate is filled in automatically when adding a new vehicle to the directory Vehicle registration, access to which is opened via a hyperlink of the same name from the settings form for calculating and charging transport tax (section Directories - Transport tax). In the form of a directory element it is necessary to indicate the OKTMO code, vehicle type code and tax base (Fig. 1). The tax base for transport tax is the engine power in horsepower (hp). If in the vehicle title the engine power is indicated only in kilowatts (kW), then it must be converted into horsepower by multiplying by a factor of 1.35962. The resulting result must be rounded to the second decimal place (clause 19 of the Methodological Recommendations for the Application of Chapter 28 of the Tax Code of the Russian Federation).

Regional law may establish differentiated rates (depending on the environmental class and age of the car), as well as benefits for the payment of transport tax. If in a subject of the federation the rate is set taking into account the number of years that have passed since the year of manufacture of the vehicle, then in the form Vehicle registration you need to set the appropriate flag, and fill out the field in the card of this fixed asset Release date (built) on the bookmark Additionally(Fig. 2).

The tax is automatically calculated for each vehicle based on the data specified in the directory Vehicle registration, including the tax rate automatically determined by the program. Calculation of the amount of transport tax (advance payments for transport tax) and reflection of the accrued amount in accounting is carried out using the routine operation of closing the month Calculation of transport tax. |

New

- Transport tax accrued (accounting entries) Transport tax rate in 1s 8

- Characteristics of a Taurus woman by zodiac sign: a gorgeous and sophisticated lady Taurus girls in relationships

- Love horoscope for Libra - rat Horoscope for April Libra water rat and

- I dreamed that I had a big belly

- Why do you dream about your parents getting divorced? I had a dream that my parents were getting divorced.

- Slavic runes, designation and interpretation

- Pisces will be helped by a person from the past, and lions will overcome the trials of fate

- Functions of the general agent for servicing public debt

- Other income - what is it?

- Tax burden coefficient Tax burden by type of economic activity in percent